How INPRS Fits Into Your Retirement

If you’re an K-12 educator in Indiana, I can’t stress enough how important the Indiana teacher pension (INPRS) is to your retirement. I’m sure you’re thinking, “wow, that’s a no brainer, of course it’s a big deal.” But in reality, you’d be surprised how many educators are unfamiliar with how it works, what they should be doing, and how to incorporate it into their retirement plans.

If you’re an K-12 educator in Indiana, I can’t stress enough how important the Indiana teacher pension (INPRS) is to your retirement. I’m sure you’re thinking, “wow, that’s a no brainer, of course it’s a big deal.” But in reality, you’d be surprised how many educators are unfamiliar with how it works, what they should be doing, and how to incorporate it into their retirement plans.

Your INPRS pension is a HUGE piece of your retirement plan! So, understanding it and what options are available is essential to making it work for you.

How Does INPRS Work?

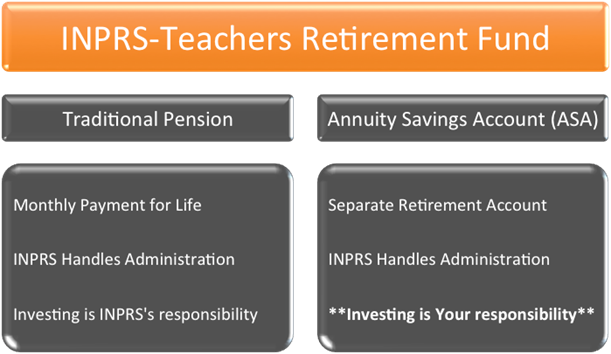

INPRS is what’s called a hybrid pension plan and it’s made up of two parts: a Traditional Pension and an Annuity Savings Account.

The traditional pension is just what you’d expect. When you retire, INPRS will pay you a monthly retirement benefit based on a calculation that incorporates multiple factors. They take care of everything from administration to investing, so there’s not much you need to do until you get close to retiring.

The Annuity Savings Account (ASA) is different and is like having a separate retirement account with INPRS. It’s mandated that 3% of your salary be contributed to it each year, and typically your district does that your behalf. Over your career, the goal is for the account balance to grow so at retirement it’s available for you to use. Here’s the surprise for many educators, investing the ASA is the teacher’s responsibility.

The Overlooked ASA

I have a feeling I know what you might be thinking… and yes, if you’ve never logged into INPRS to designate how your ASA funds should be invested, they’re sitting there in the Stable Value Fund right now. (To be clear, the Stable Value Fund earns very little). Over a 30-year career, having your money in the Stable Value Fund vs being invested can cost you tens of thousands of dollars in potential earnings.

Now, INPRS has done a good job making it easy to designate and manage the investments in your ASA. All you need to do is create an INPRS log-in and passcode at https://www4.benefitsweb.com/inprs.html. Once you’re in, navigate to the “My Account” tab, and then you’ll see “Investments”. Once there, you’ll be able to designate investments for your current funds and set up your account so future contributions are invested as they’re made.

Available investment options for ASAs include seven funds representing specific asset classes and a suite of target date funds. Since we’re on the subject, I always like to remind clients that it’s important to coordinate your ASA investments with any other retirement accounts you have to ensure a consistent investing approach.

If you're not sure what to do and need help deciding how you should invest, contact us, we’re happy to walk you through the process and set up an investment allocation that works for you. INPRS also provides several resources on investing basics on their website. (INPRS Investment Education).

So, before we go any further… if you’ve never designated the investments for your ASA, put it on your to-do list. It’s also important to take a moment during this time to name a beneficiary for your ASA, which is also done through your INPRS portal.

Options at Retirement - Pension

Now, let’s look at the options for your traditional pension payment. INPRS calculates the monthly payment you’ll receive using five factors:

- Your five highest yearly salaries

- Your Years of Service

- Your age at retirement

- A benefit multiplier of 1.1%

- The payment option you select (more on this in a moment)

For example, the benefit for a teacher who meets the regular retirement requirement, has 30 years of service, and a five highest years of salary average of $70,000 would be calculated as:

| Highest Five Years Salary (Average): | $70,000 |

| Benefit Multiplier (1.1%) | x0.011 |

| (equals Pension Base) | $770 |

| Years of Service | x 30 |

| (equals Annual Retirement Benefit) | $23,100 |

| Monthly Benefit | / 12 |

| Calculated benefit (option A-1) | $1,925 |

You may notice “(option A-1)” in the line above. That specifies the payment option. In the traditional pension, there are seven options to choose from, each guaranteeing something different. Figuring out which is right for you depends on answering a few questions like:

- Do you have longevity in your family?

- How’s your health?

- Are you married?

- Do you need/want to ensure your survivor(s) receive payments after your death?

- Full or partial survivor payments?

Your situation is unique, so choosing the payment option that will work best with your retirement plan is important. Each has a different effect on your monthly benefit. For our example teacher, the other options available for her payment range from $1,657-$1,941 per month. You are allowed to change options down the road, however, your first choice will affect any future options, so it’s wise to make it count.

Options at Retirement – ASA

Finally, let’s take a look at the options available for your ASA at retirement. At this point in time, hopefully it will have grown into a substantial sum. Practically speaking, there are four main options available:

Finally, let’s take a look at the options available for your ASA at retirement. At this point in time, hopefully it will have grown into a substantial sum. Practically speaking, there are four main options available:

Monthly ASA: In this option, you have the ability to annuitize your ASA funds to provide a monthly payment similar to your pension payment. Currently, INPRS manages this, however, beginning January 1, 2018, they will begin partnering with MetLife to provide fixed annuities for this option. Similar to the traditional pension payment, you will need to elect a payment option based on the same questions in the previous section.

I’ve seen many educators choose this option because it seems like a simple solution. However, annuities are complex and don’t forget that once you choose to annuitize and begin receiving monthly payments those funds go to the insurance company and are no longer yours. This removes any chance of being able to go-back and try again or provide flexibility if your situation changes down the road.

Full or Partial Withdrawal: This option allows you to fully or partially withdrawal from your ASA account. ASA funds were contributed pre-tax, so that means any withdrawals you take will be subject to income taxes. Also, once the funds have been withdrawn they cannot be put back in to regain their tax-deferred status.

It can be dangerous to take this option, especially without considering or properly planning for the tax consequences. It’s also important to know how your ASA funds fit into the overall coordination of all your retirement accounts because you may not need to withdrawal any of them immediately at retirement.

Deferment: This option allows you to leave your ASA funds in your account, invested how you choose. If you find yourself in a situation where based on your retirement plan you won’t need to take withdrawals or income from your ASA, it might be best just to continue as is.

Remember, since your ASA is a tax deferred retirement account, it will be subject to Required Minimum Distributions starting the year in which you turn 70 ½.

Direct Rollover: This option allows you to roll over the balance of your ASA to another retirement account. Doing this preserves the tax-deferred status of the funds and can provide two major benefits. First, as we examined earlier, ASAs have limited investment choices. Rolling the funds into another retirement account could provide you with a much wider range of investment options.

Second, many people find it’s convenient to consolidate their accounts when they retire because it makes coordinating investment strategy, tax decisions, and required minimum distributions an easier process. This could be done if you already have a Traditional IRA and/or a 403(b) you also used to save for retirement.

Make sure you carefully evaluate the options and consider the consequences before you select the option for your ASA. Unlike the traditional pension payments that can change, the option you choose for your ASA will likely be permanent.

Moving Forward

I hope this article has provided you with a good understanding of how INPRS fits into your retirement and how truly important your are decisions regarding your accout. It’s a unique benefit that if utilized to its potential can serve your well throughout your golden years. Make sure you take advantage of it!

We’d love to hear from you and provide more information on how we can help with your retirement planning, including making the most of your INPRS benefits.Schedule an Introduction

Don’t forget to follow us on Facebook, Twitter, and LinkedIn for more important updates and tips on financial planning for teachers and families with special needs!

Mychal Eagleson, CFP®, AAMS® is the President of An Exceptional Life Financial, a firm that specializes in financial planning for teachers and families with special needs. He frequently writes and speaks on personal finance topics relating to these clients. Mychal also serves on the board of the Financial Planning Association of Greater Indiana as the Director of Public Relations & Social Media. To read more of his articles or learn about An Exceptional Life Financial please

Mychal Eagleson, CFP®, AAMS® is the President of An Exceptional Life Financial, a firm that specializes in financial planning for teachers and families with special needs. He frequently writes and speaks on personal finance topics relating to these clients. Mychal also serves on the board of the Financial Planning Association of Greater Indiana as the Director of Public Relations & Social Media. To read more of his articles or learn about An Exceptional Life Financial please